Australians Are Throwing Away Too Much Food / オーストラリアでは食品ロスが多すぎる?

yamanami-1023

Australia Through Japanese Eyes

In my previous post I explained why OVHC (Overseas Visitors Health Cover) matters for moving to Australia (often mandatory for temporary visas).

This time, I actually requested free quotes on official sites to get a feel for the coverage and pricing.

前回の記事で、オーストラリア移住には OVHC(Overseas Visitor Health Cover) が重要(多くの一時ビザで必須)と書きました。

今回は、公式サイトで無料見積もりを実際に試し、カバー内容と金額感の雰囲気をつかんでみました。

The purpose here is not to decide now, but to grasp price range + how coverage is shown.

今回の目的は“今決める”ことではなく、金額感とカバーの見え方をつかむこと。

以下の3つの有名な保険会社を調べました。

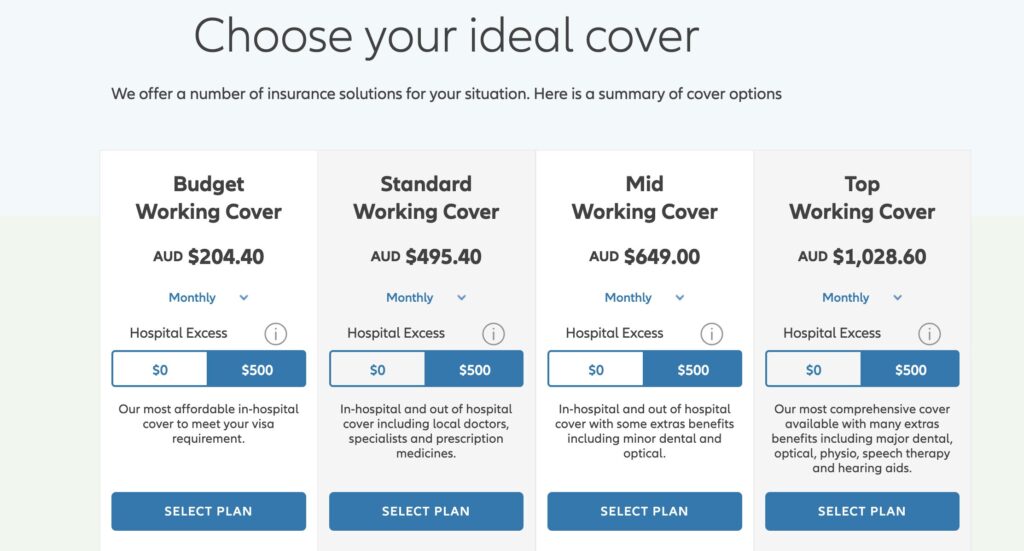

Open the Allianz OVHC page and enter visa type, family numbers, start/end dates, and age band.

AllianzのOVHCページ を開き、ビザ種別・人数・開始/終了日・年齢帯を入れると、週/月/年の金額とプラン比較表がすぐ表示されます。

A weekly/monthly/annual price table appears instantly, and it’s easy to tweak inputs and re-calculate.

条件を変えての再計算もしやすく、迷いにくいUIでした。

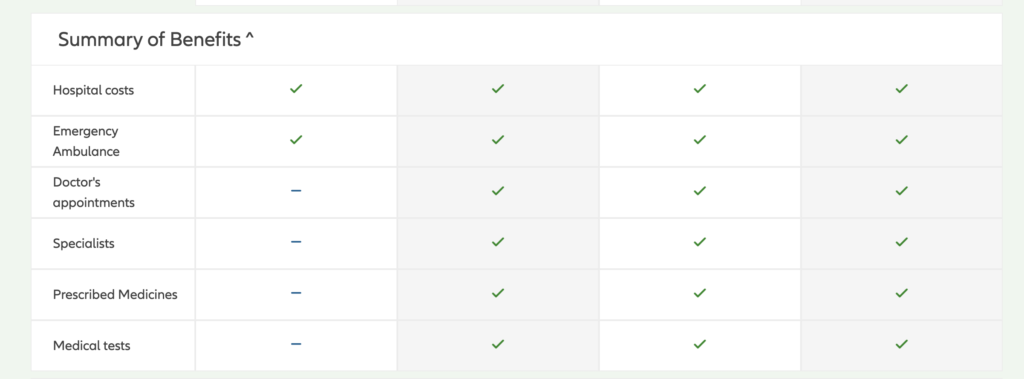

Coverage varies by plan, but generally includes the following:

プランにより差はあるものの、一般的には次のような領域をカバーします:

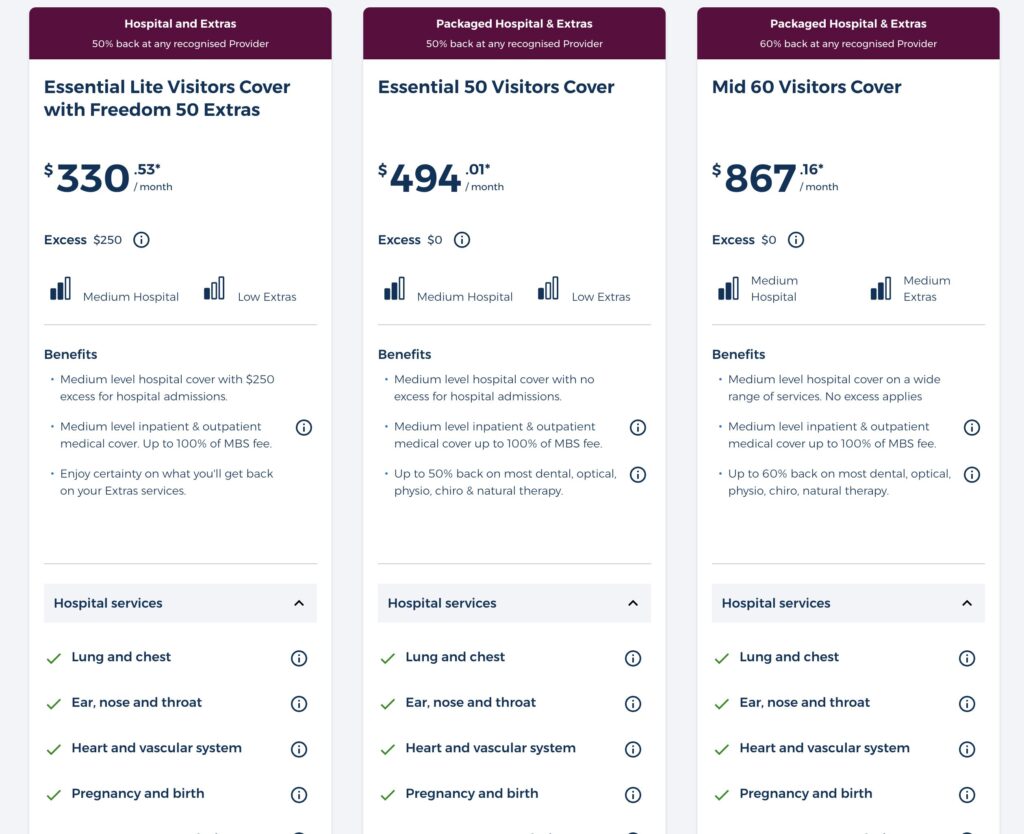

I quoted with our family details (36/48/1) and VIC. What affected the price most was the Excess ($0 vs $250…) and the Extras rebate rate (50% or 60%).

家族(36歳/48歳/1歳)・VICで見積もり。Excess($0か$250かなど) と Extrasの戻り率(50%/60%) の違いで、月額が大きく動く印象でした。

Ballpark from my screen (with my conditions):

おおよその金額感(今回の条件例):

*Varies by age/state/people/start month.)

年齢・州・人数・開始月 などで大きく変わります。

Medibank’s first quote view is often Hospital + Medical (Extras separate), so next to Bupa’s Hospital+Extras packages it can look cheaper. Also, choosing a higher Excess (A$0 / 250 / 500 / 750…) lowers premiums.

Medibankは初期表示がHospital+Medical(Extras別)のことが多く、Hospital+Extras込みで出るBupaと並べると安く見えやすいです。さらに Excess(A$0/250/500/750…) を上げるほど保険料は下がります。

Note on “Your government rebate”

:When you enter your conditions while filling out the quote form, you can see “”That message is for Medicare-eligible residents; OVHC members are generally not eligible, so you can ignore it when quoting.

見積もり入力中に出てきます。

これはMedicare対象の居住者向け補助の説明で、OVHCは基本対象外。見積もりではスルーで大丈夫です。

Quotes took just a few minutes and lowered the mental hurdle.

Because prices and promos change, it’s best to run fresh quotes. With my family setup (36/58/1 in VIC), I’m roughly holding Basic ≈ A$300/mo, Mid ≈ A$500/mo, Comprehensive ≈ A$1,000/mo as a working feel.

When we get closer to moving, I’ll compare networks and Extras in detail.

見積もりは数分で完了し、心理的ハードルが下がりました。

料金改定やキャンペーンがあるため、最新画面で再見積もりするのがいちばん確実です。

今回の家族条件(36/58/1、VIC)では、ベーシック約A$300/中位約A$500/厚め約A$1,000を当面の目安にします。

移住が近づいたらネットワークやExtrasまで含めて本格比較しようと思います。

Disclaimer(免責メモ)

Prices vary by visa type, cover level, ages, family size, period, and state. Annual premium reviews also apply. Treat figures here as indicative only—always confirm via each insurer’s latest quote.

料金はビザ種別・カバー水準・年齢・人数・期間・州などで変動し、年度改定もあります。本記事の金額は参考情報です。必ず各社の最新見積もりでご確認ください。

コメントを残す